Federal Reserve (Fed) Chair Jerome Powell said last month’s decision to cut the fed funds target rate by a half percentage point was due to a “recalibrating” policy, as the Fed follows its dual mandate regarding inflation and growth.

The new buzzword — recalibration — implies mechanical fine-tuning, but unfortunately, the macro economy is not that robotic. We are full of emotional people with ever-changing needs and wants. However, the buzzword also evokes something therapeutic; that is, the Fed is not cutting rates because of an imminent recession. In fact, the economy will likely grow above trend for yet another quarter or two. However, risks are rising for 2025.

Blowout Payrolls, or Was It?

We do not believe the Fed is cutting rates because a recession is just around the corner but rather because rates are still too restrictive. Yes, a slowdown looks likely next year, but for now, businesses are benefitting from a consumer on very good footing with higher income growth coupled with more savings. More on that in later paragraphs.

September payrolls rose 254,000, higher than the annual monthly average of 203,000 and fairly broad- based. Payrolls increased in most sectors such as restaurants, healthcare, construction, and government, pulling the unemployment rate down slightly to 4.1%. Average hourly earnings rose 0.4% from a month ago, now up 4% from a year ago. Real purchasing power continues to increase, which is good news for businesses and consumers.

Hours worked edged down to 34.2 hours in September and trending below the pre-pandemic average. This is an important metric for growth and productivity forecasts.

One cautionary flag could be the rise in those with multiple jobs. The percentage of individuals holding multiple jobs rose to 5.3%. The previous time this ratio was higher was in early 2009, when the economy was in the midst of the Great Financial Crisis. A further note to dampen the exuberance is the year-over-year change in the non-seasonally adjusted data reveal a very orderly and consistent slowdown, including this latest monthly release. And October’s data will probably not be as strong due to the Boeing strike and the impact from Hurricane Helene. Nonetheless, the data supports the soft-landing narrative, especially with the revisions to income and savings we will cover in a moment.

The bottom line is this solid report increases the odds that the economy will continue to grow above trend in the next quarter. Our base case is the Fed will cut by a quarter-point at the next few meetings. Further, this solid payroll report validates any potential half-point reduction in fed funds was completely unwarranted.

Fed funds futures market is responding accordingly.

Trouble at the Docks

For the first time since 1977, members of the International Longshoremen’s Association (ILA) went on strike, putting a wrinkle in the Fed’s best-laid plans to ease policy rates without instigating a resurgence of inflation. Thankfully, the strike only lasted three days, but the effects could linger. The ILA agreed on October 3 to extend their contract that had expired on September 30 until mid-January, setting the economy up for another potential conflict next year.

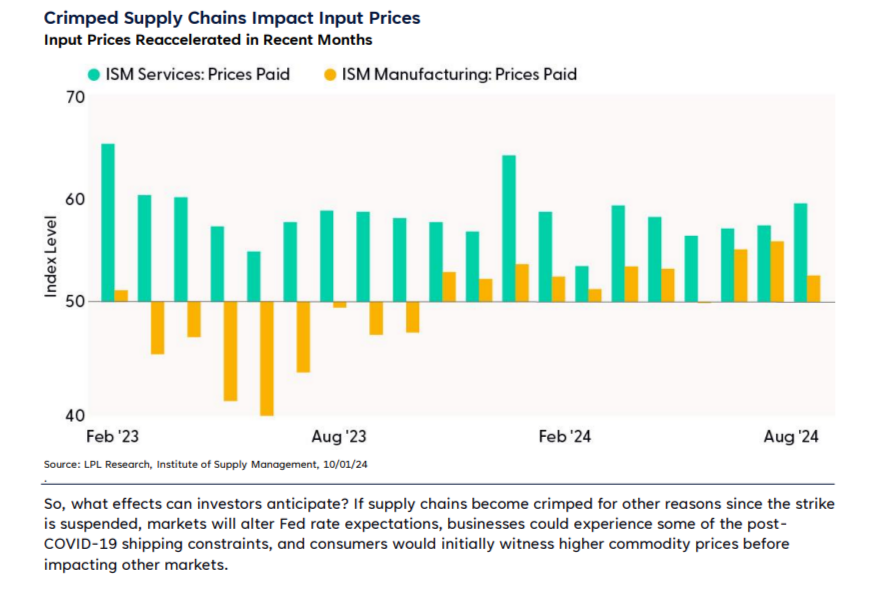

The recent longshoreman strike affected 40 ports to various degrees across the country, and if it had lasted a week, some estimated it would have cost over $2 billion in lost business.¹ In a separate dispute, the Boeing machinist strike has lasted three weeks so far, costing the economy over $1 billion and adding to the fragilities of the market. Although only a few days long, the port strike impacted perishable items, according to the American Farm Bureau Federation. These strikes added tension to an already-stressed supply chain, increasing input prices paid by businesses.

Independent of the union drama, supply pressures had previously increased in August, so the strike’s effects could linger for a bit. According to the Institute of Supply Management, businesses reported a reacceleration of input costs before the strikes, so if supply chains tighten further by other means, consumers will eventually notice an uptick in prices. In the chart below, a value greater than 50 implies expanding prices.

But Consumers Have Buffers

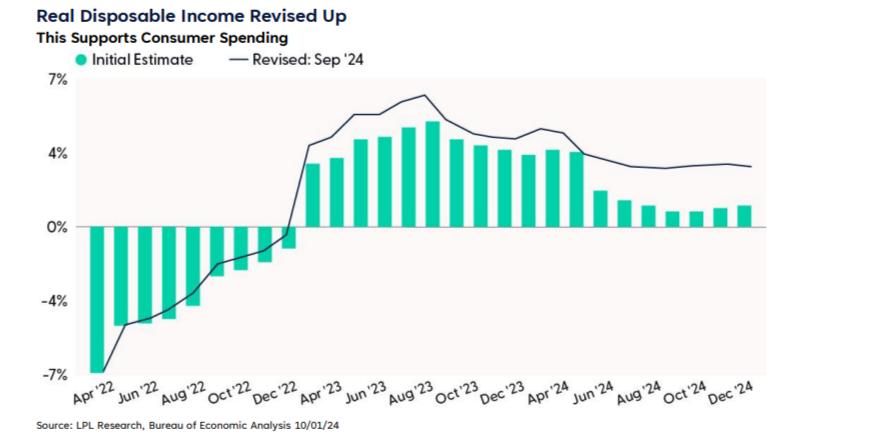

Inflation-adjusted disposable income, which is after taxes and social insurance payments, grew much faster over the past 24 months than originally thought. As shown below, as a consequence of high labor demand and plenty of job-switching, workers saw their wages and salaries grow faster than inflation for the past two years. This explains why consumers have had the ability to spend despite high price levels.

Savings Not So Depleted

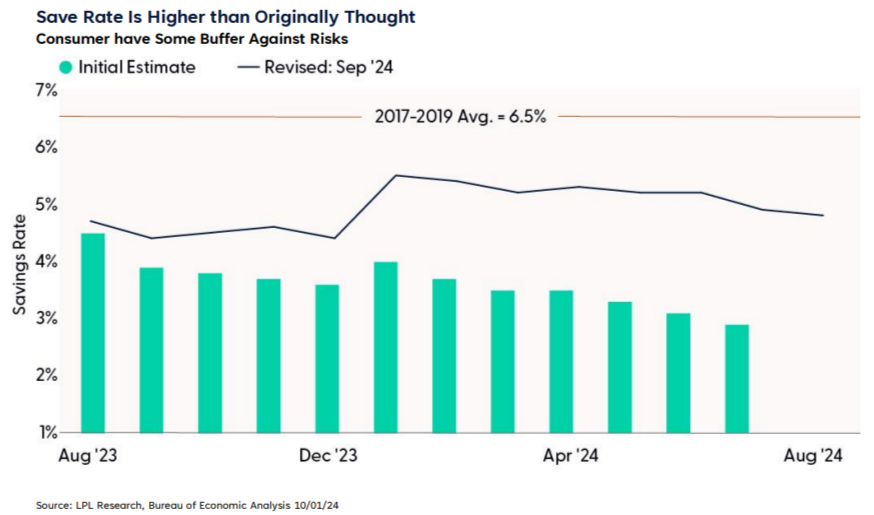

Earlier this year, one of the growing concerns among investors was the unknown impact of depleted savings. But after the recent income and spending revisions, consumers are saving a lot more than originally estimated.

If disposable incomes grew faster than originally thought and real spending also grew but at a slower pace, then by definition, consumers now have a larger portion of their money in savings. This chart shows the improved amount of savings consumers have on their balance sheets. Just take this past July, for example. The initial estimate for July’s personal savings rate was 2.9%, but after a more complete analysis, consumers’ personal savings rate was revised up to roughly 5%. This is getting close to the pre-pandemic average of 6.5%. A higher savings rate means consumers have a bit more buffer to manage any potential shocks.

Quits, Layoffs, and Openings

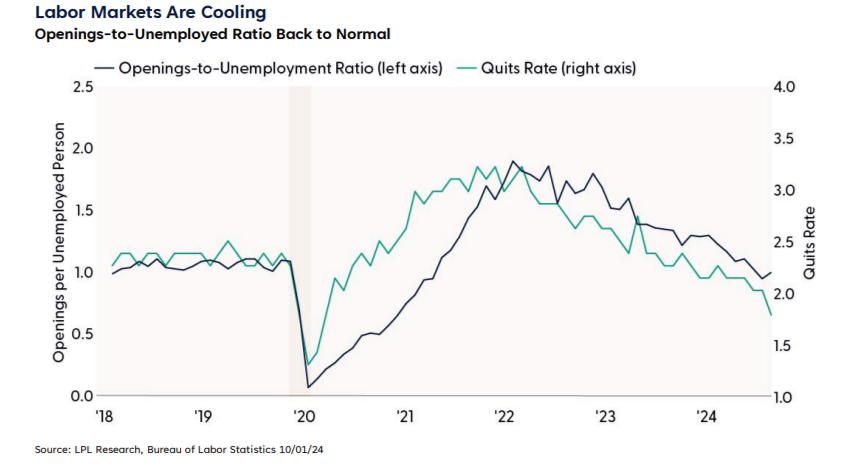

One recently popular way to measure tightness in the job market is to consider the ratio of job openings to those looking for work, the openings-to-unemployed ratio. The Job Opening and Labor Turnover Survey (JOLTS) provides a prime example of a data set that was previously ignored but in the recent tightening cycle, became a fixation for policy makers. As investors remember, Chairman Powell made much of the Openings-to-Unemployed ratio at the beginning of the tightening cycle of 2022. That ratio was highly watched, dissected, and debated, but goes back a decade or so, and traders often ignored that JOLTS release. The lag in publication date was a reason JOLTS was often marginalized.

However, the Openings-to-Unemployed Ratio rose in August, but still at pre-COVID 19 norms. In a separate line item, the quits rate for lower-skilled workers fell to the lowest in roughly a decade as these workers were less inclined to quit amid a slowing job market.

Employment demand is slowing, especially in the manufacturing sector, as firms are implementing hiring freezes. As the data unfold, we expect the Fed will likely cut by a quarter-point at each of the remaining meetings this year, unless we experience unexpected deteriorating conditions.

Artificial Intelligence Motivated Layoff Announcements

Many workers are befuddled with the impact from artificial intelligence on the workforce. A simple maxim is “AI won’t replace humans – but humans with AI will replace humans without AI.” 2 The spike in September layoff announcements was motivated by firms implementing more artificial intelligence, according to the latest report from Challenger, Gray and Christmas, a company which tracks layoff announcements by reason, industry, and geography. The telecommunication industry announced significant layoffs in September, causing the overall announced job cuts to spike this month. Job cuts in the insurance sector rose the highest since 2020 as this industry is recalibrating post-pandemic. Retail and transportation firms have fewer hiring plans this year relative to last year despite entering the holiday season. Hiring plans over the past few months were significantly lower than a year ago, validating the slowing labor market.

Rising job cut announcements coupled with fewer hiring plans indicate businesses are hesitant about adding to their payrolls.

Conclusion

Fed rate-cuts in September boosted stocks during what has been a historically weak month for stocks, but after five straight positive months, we would not be surprised if we witness at least a consolidation in October as markets take a breath ahead of the election. In general, October has proven more of a treat than a trick for stock markets, as we recently published on our blog, but in U.S. presidential election years, the month can be a little scary for investors as markets struggle to come to terms with election-related volatility.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) continues to maintain its tactical neutral stance on equities. However, we do not rule out the possibility of short-term weakness, especially as geopolitical threats in the Middle East escalate. Equities may also readjust to what we expect will be a slower and shallower Fed rate-cutting cycle than markets are currently pricing in, although both post- election and fourth-quarter seasonality are favorable for stocks.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent

or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

All index data from Bloomberg.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Tracking #640855 (Exp. 10/25)

https://www.andersoneconomicgroup.com/ila-strike-against-ports-along-east-gulf-coasts-potential-week-1-losses-estimated-at-2-1-billion/

https://hbr.org/2023/08/ai-wont-replace-humans-but-humans-with-ai-will-replace-humans-without-ai/

Just When We Recalibrated, Another Shock Arrive

Blowout Payrolls, or Was It?

We do not believe the Fed is cutting rates because a recession is just around the corner but rather because rates are still too restrictive. Yes, a slowdown looks likely next year, but for now, businesses are benefitting from a consumer on very good footing with higher income growth coupled with more savings. More on that in later paragraphs.

September payrolls rose 254,000, higher than the annual monthly average of 203,000 and fairly broad- based. Payrolls increased in most sectors such as restaurants, healthcare, construction, and government, pulling the unemployment rate down slightly to 4.1%. Average hourly earnings rose 0.4% from a month ago, now up 4% from a year ago. Real purchasing power continues to increase, which is good news for businesses and consumers.

Hours worked edged down to 34.2 hours in September and trending below the pre-pandemic average. This is an important metric for growth and productivity forecasts.

One cautionary flag could be the rise in those with multiple jobs. The percentage of individuals holding multiple jobs rose to 5.3%. The previous time this ratio was higher was in early 2009, when the economy was in the midst of the Great Financial Crisis. A further note to dampen the exuberance is the year-over-year change in the non-seasonally adjusted data reveal a very orderly and consistent slowdown, including this latest monthly release. And October’s data will probably not be as strong due to the Boeing strike and the impact from Hurricane Helene. Nonetheless, the data supports the soft-landing narrative, especially with the revisions to income and savings we will cover in a moment.

The bottom line is this solid report increases the odds that the economy will continue to grow above trend in the next quarter. Our base case is the Fed will cut by a quarter-point at the next few meetings. Further, this solid payroll report validates any potential half-point reduction in fed funds was completely unwarranted.

Fed funds futures market is responding accordingly.

Trouble at the Docks

For the first time since 1977, members of the International Longshoremen’s Association (ILA) went on strike, putting a wrinkle in the Fed’s best-laid plans to ease policy rates without instigating a resurgence of inflation. Thankfully, the strike only lasted three days, but the effects could linger. The ILA agreed on October 3 to extend their contract that had expired on September 30 until mid-January, setting the economy up for another potential conflict next year.

The recent longshoreman strike affected 40 ports to various degrees across the country, and if it had lasted a week, some estimated it would have cost over $2 billion in lost business.¹ In a separate dispute, the Boeing machinist strike has lasted three weeks so far, costing the economy over $1 billion and adding to the fragilities of the market. Although only a few days long, the port strike impacted perishable items, according to the American Farm Bureau Federation. These strikes added tension to an already-stressed supply chain, increasing input prices paid by businesses.

Independent of the union drama, supply pressures had previously increased in August, so the strike’s effects could linger for a bit. According to the Institute of Supply Management, businesses reported a reacceleration of input costs before the strikes, so if supply chains tighten further by other means, consumers will eventually notice an uptick in prices. In the chart below, a value greater than 50 implies expanding prices.

But Consumers Have Buffers

Inflation-adjusted disposable income, which is after taxes and social insurance payments, grew much faster over the past 24 months than originally thought. As shown below, as a consequence of high labor demand and plenty of job-switching, workers saw their wages and salaries grow faster than inflation for the past two years. This explains why consumers have had the ability to spend despite high price levels.

Savings Not So Depleted

Earlier this year, one of the growing concerns among investors was the unknown impact of depleted savings. But after the recent income and spending revisions, consumers are saving a lot more than originally estimated.

If disposable incomes grew faster than originally thought and real spending also grew but at a slower pace, then by definition, consumers now have a larger portion of their money in savings. This chart shows the improved amount of savings consumers have on their balance sheets. Just take this past July, for example. The initial estimate for July’s personal savings rate was 2.9%, but after a more complete analysis, consumers’ personal savings rate was revised up to roughly 5%. This is getting close to the pre-pandemic average of 6.5%. A higher savings rate means consumers have a bit more buffer to manage any potential shocks.

Quits, Layoffs, and Openings

One recently popular way to measure tightness in the job market is to consider the ratio of job openings to those looking for work, the openings-to-unemployed ratio. The Job Opening and Labor Turnover Survey (JOLTS) provides a prime example of a data set that was previously ignored but in the recent tightening cycle, became a fixation for policy makers. As investors remember, Chairman Powell made much of the Openings-to-Unemployed ratio at the beginning of the tightening cycle of 2022. That ratio was highly watched, dissected, and debated, but goes back a decade or so, and traders often ignored that JOLTS release. The lag in publication date was a reason JOLTS was often marginalized.

However, the Openings-to-Unemployed Ratio rose in August, but still at pre-COVID 19 norms. In a separate line item, the quits rate for lower-skilled workers fell to the lowest in roughly a decade as these workers were less inclined to quit amid a slowing job market.

Employment demand is slowing, especially in the manufacturing sector, as firms are implementing hiring freezes. As the data unfold, we expect the Fed will likely cut by a quarter-point at each of the remaining meetings this year, unless we experience unexpected deteriorating conditions.

Artificial Intelligence Motivated Layoff Announcements

Many workers are befuddled with the impact from artificial intelligence on the workforce. A simple maxim is “AI won’t replace humans – but humans with AI will replace humans without AI.” 2 The spike in September layoff announcements was motivated by firms implementing more artificial intelligence, according to the latest report from Challenger, Gray and Christmas, a company which tracks layoff announcements by reason, industry, and geography. The telecommunication industry announced significant layoffs in September, causing the overall announced job cuts to spike this month. Job cuts in the insurance sector rose the highest since 2020 as this industry is recalibrating post-pandemic. Retail and transportation firms have fewer hiring plans this year relative to last year despite entering the holiday season. Hiring plans over the past few months were significantly lower than a year ago, validating the slowing labor market.

Rising job cut announcements coupled with fewer hiring plans indicate businesses are hesitant about adding to their payrolls.

Conclusion

Fed rate-cuts in September boosted stocks during what has been a historically weak month for stocks, but after five straight positive months, we would not be surprised if we witness at least a consolidation in October as markets take a breath ahead of the election. In general, October has proven more of a treat than a trick for stock markets, as we recently published on our blog, but in U.S. presidential election years, the month can be a little scary for investors as markets struggle to come to terms with election-related volatility.

Asset Allocation Insights

LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) continues to maintain its tactical neutral stance on equities. However, we do not rule out the possibility of short-term weakness, especially as geopolitical threats in the Middle East escalate. Equities may also readjust to what we expect will be a slower and shallower Fed rate-cutting cycle than markets are currently pricing in, although both post- election and fourth-quarter seasonality are favorable for stocks.

Important Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent

or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

All index data from Bloomberg.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Tracking #640855 (Exp. 10/25)

https://www.andersoneconomicgroup.com/ila-strike-against-ports-along-east-gulf-coasts-potential-week-1-losses-estimated-at-2-1-billion/

https://hbr.org/2023/08/ai-wont-replace-humans-but-humans-with-ai-will-replace-humans-without-ai/